1. Exogenous variables

Exogenous variables are external factors that provide additional information about the behavior of the target variable in time series forecasting. These variables, which are correlated with the target, can significantly improve predictions. Examples of exogenous variables include weather data, economic indicators, holiday markers, and promotional sales.

TimeGPT allows you to include exogenous variables when

generating a forecast. This vignette will show you how to include them.

It assumes you have already set up your API key. If you haven’t done

this, please read the Get

Started vignette first.

2. Load data

For this vignette, we will use the electricity consumption dataset

with exogenous variables included in nixtlar. This dataset

contains hourly prices from five different electricity markets, along

with two exogenous variables related to the prices and binary variables

indicating the day of the week.

df_exo_vars <- nixtlar::electricity_exo_vars

head(df_exo_vars)

#> unique_id ds y Exogenous1 Exogenous2 day_0 day_1 day_2

#> 1 BE 2016-10-22 00:00:00 70.00 49593 57253 0 0 0

#> 2 BE 2016-10-22 01:00:00 37.10 46073 51887 0 0 0

#> 3 BE 2016-10-22 02:00:00 37.10 44927 51896 0 0 0

#> 4 BE 2016-10-22 03:00:00 44.75 44483 48428 0 0 0

#> 5 BE 2016-10-22 04:00:00 37.10 44338 46721 0 0 0

#> 6 BE 2016-10-22 05:00:00 35.61 44504 46303 0 0 0

#> day_3 day_4 day_5 day_6

#> 1 0 0 1 0

#> 2 0 0 1 0

#> 3 0 0 1 0

#> 4 0 0 1 0

#> 5 0 0 1 0

#> 6 0 0 1 0There are two types of exogenous variables: historic and future.

-

Historic Exogenous Variables: They should be

included directly in the input dataset

df.

-

Future Exogenous Variables: They must be included

in the

X_dfparameter.

To specify which variables should be treated as historic, use the

hist_exog_list parameter. This parameter is available in

both the forecast and cross_validation

functions.

- If

dfcontains exogenous variables but they are not found inX_dfnor declared inhist_exog_list, they will be ignored.

- If exogenous variables were declared as historic but found in

X_df, then they will be considered as historic.

In the next section, we will explore different cases for forecasting with exogenous variables.

3a. Forecasting electricity prices using historic and future exogenous variables

If both historic and future values of all exogenous variables are

available, include the historic exogenous variables in df

and the future exogenous variables in X_df.

future_exo_vars <- nixtlar::electricity_future_exo_vars

head(future_exo_vars)

#> unique_id ds Exogenous1 Exogenous2 day_0 day_1 day_2 day_3

#> 1 BE 2016-12-31 00:00:00 64108 70318 0 0 0 0

#> 2 BE 2016-12-31 01:00:00 62492 67898 0 0 0 0

#> 3 BE 2016-12-31 02:00:00 61571 68379 0 0 0 0

#> 4 BE 2016-12-31 03:00:00 60381 64972 0 0 0 0

#> 5 BE 2016-12-31 04:00:00 60298 62900 0 0 0 0

#> 6 BE 2016-12-31 05:00:00 60339 62364 0 0 0 0

#> day_4 day_5 day_6

#> 1 0 1 0

#> 2 0 1 0

#> 3 0 1 0

#> 4 0 1 0

#> 5 0 1 0

#> 6 0 1 0

fcst_exo_vars <- nixtla_client_forecast(

df_exo_vars,

h = 24,

X_df = future_exo_vars

)

#> Frequency chosen: h

#> Using future exogenous features: [Exogenous1, Exogenous2, day_0, day_1, day_2, day_3, day_4, day_5, day_6]

head(fcst_exo_vars)

#> unique_id ds TimeGPT

#> 1 BE 2016-12-31 00:00:00 74.54077

#> 2 BE 2016-12-31 01:00:00 43.34429

#> 3 BE 2016-12-31 02:00:00 44.42921

#> 4 BE 2016-12-31 03:00:00 38.09440

#> 5 BE 2016-12-31 04:00:00 37.38914

#> 6 BE 2016-12-31 05:00:00 39.085743b. Forecasting electricity prices using only historic exogenous variables

If future values of the exogenous variables are not available, you

can still generate forecasts using only their historical values. In this

case, simply include them in df and declare them in

hist_exog_list.

fcst_exo_vars <- nixtla_client_forecast(

df_exo_vars,

h = 24,

hist_exog_list = c("Exogenous1", "Exogenous2", "day_0", "day_1", "day_2", "day_3", "day_4", "day_5", "day_6")

)

#> Frequency chosen: h

#> Using historical exogenous features: [Exogenous1, Exogenous2, day_0, day_1, day_2, day_3, day_4, day_5, day_6]

head(fcst_exo_vars)

#> unique_id ds TimeGPT

#> 1 BE 2016-12-31 00:00:00 45.76938

#> 2 BE 2016-12-31 01:00:00 47.99101

#> 3 BE 2016-12-31 02:00:00 49.49613

#> 4 BE 2016-12-31 03:00:00 49.51081

#> 5 BE 2016-12-31 04:00:00 48.51056

#> 6 BE 2016-12-31 05:00:00 50.20716Note that if you don’t declare the exogenous variables in

hist_exog_list, they will be ignored. If we hadn’t declared

them above, the output would be the same as the TimeGPT forecast using

only the target variable y.

Important: If you include historical exogenous variables without explicitly defining their future values, you are implicitly assuming that their historical patterns will continue into the future. Whenever possible, it is recommended to use future exogenous variables to make these assumptions explicit.

3c. Forecasting future exogenous variables

When future exogenous variables are not available, an alternative

approach is to forecast them separately using TimeGPT. First, generate

forecasts for the exogenous variables and then pass the predicted values

in X_df for the main forecast.

3d. Forecasting electricity prices using both future and historic exogenous variables

In some cases, only a subset of future exogenous variables is

available. For example, if future values of Exogenous1 and

Exogenous2 are unknown, add them to

hist_exog_list.

future_exo_vars <- future_exo_vars |>

dplyr::select(-dplyr::all_of(c("Exogenous1", "Exogenous2")))

fcst_exo_vars <- nixtla_client_forecast(

df_exo_vars,

h = 24,

X_df = future_exo_vars,

hist_exog_list = c("Exogenous1", "Exogenous2")

)

#> Frequency chosen: h

#> The following features were declared as historic but found in X_df:: [Exogenous1, Exogenous2]. They will be considered historic.

#> Using future exogenous features: [day_0, day_1, day_2, day_3, day_4, day_5, day_6]

#> Using historical exogenous features: [Exogenous1, Exogenous2]

head(fcst_exo_vars)

#> unique_id ds TimeGPT

#> 1 BE 2016-12-31 00:00:00 47.05948

#> 2 BE 2016-12-31 01:00:00 49.28110

#> 3 BE 2016-12-31 02:00:00 50.78623

#> 4 BE 2016-12-31 03:00:00 50.80090

#> 5 BE 2016-12-31 04:00:00 49.80066

#> 6 BE 2016-12-31 05:00:00 51.497254. Plot TimeGPT forecast

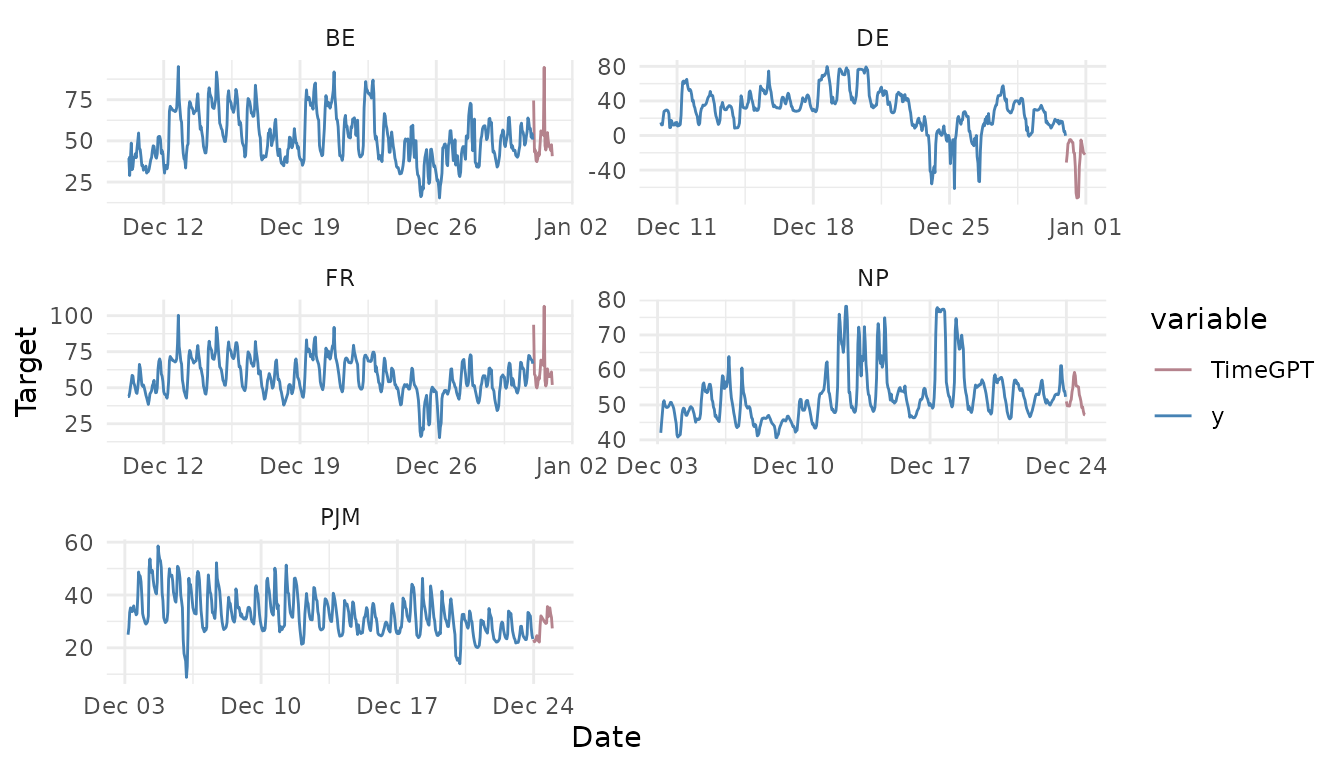

nixtlar includes a function to plot the historical data

and any output from nixtla_client_forecast,

nixtla_client_historic,

nixtla_client_anomaly_detection and

nixtla_client_cross_validation. If you have long series,

you can use max_insample_length to only plot the last N

historical values (the forecast will always be plotted in full).

nixtla_client_plot(df_exo_vars, fcst_exo_vars, max_insample_length = 500)