1. Uncertainty quantification via prediction intervals

For uncertainty quantification, TimeGPT can generate

both prediction intervals and quantiles, offering a measure of the range

of potential outcomes rather than just a single point forecast. In

real-life scenarios, forecasting often requires considering multiple

alternatives, not just one prediction. This vignette will explain how to

use prediction intervals with TimeGPT via the

nixtlar package.

A prediction interval is a range of values that the forecast can take with a given probability, often referred to as the confidence level. Hence, a 95% prediction interval should contain a range of values that includes the actual future value with a probability of 95%. Prediction intervals are part of probabilistic forecasting, which, unlike point forecasting, aims to generate the full forecast distribution instead of just the mean or the median of that distribution.

This vignette assumes you have already set up your API key. If you haven’t done this, please read the Get Started vignette first.

2. Load data

For this vignette, we will use the electricity consumption dataset

that is included in nixtlar, which contains the hourly

prices of five different electricity markets.

df <- nixtlar::electricity

head(df)

#> unique_id ds y

#> 1 BE 2016-10-22 00:00:00 70.00

#> 2 BE 2016-10-22 01:00:00 37.10

#> 3 BE 2016-10-22 02:00:00 37.10

#> 4 BE 2016-10-22 03:00:00 44.75

#> 5 BE 2016-10-22 04:00:00 37.10

#> 6 BE 2016-10-22 05:00:00 35.613. Forecast with prediction intervals

TimeGPT can generate prediction intervals when using the

following functions:

- nixtlar::nixtla_client_forecast()

- nixtlar::nixtla_client_historic()

- nixtlar::nixtla_client_detect_anomalies()

- nixtlar::nixtla_client_cross_validation()For any of these functions, simply set the level

argument to the desired confidence level for the prediction intervals.

Keep in mind that level should be a vector with numbers

between 0 and 100. You can use either quantiles or

level for uncertainty quantification, but not both.

fcst <- nixtla_client_forecast(df, h = 8, level=c(80,95))

#> Frequency chosen: h

head(fcst)

#> unique_id ds TimeGPT TimeGPT-lo-95 TimeGPT-lo-80

#> 1 BE 2016-12-31 00:00:00 45.19122 30.49719 35.50965

#> 2 BE 2016-12-31 01:00:00 43.24537 28.96447 35.37618

#> 3 BE 2016-12-31 02:00:00 41.95892 27.06669 35.34091

#> 4 BE 2016-12-31 03:00:00 39.79675 27.96763 32.32674

#> 5 BE 2016-12-31 04:00:00 39.20512 24.66191 31.00021

#> 6 BE 2016-12-31 05:00:00 40.10902 23.05225 32.43594

#> TimeGPT-hi-80 TimeGPT-hi-95

#> 1 54.87278 59.88525

#> 2 51.11456 57.52628

#> 3 48.57694 56.85116

#> 4 47.26675 51.62587

#> 5 47.41004 53.74834

#> 6 47.78209 57.16578Note that the level argument in the

nixtlar::nixtla_client_detect_anomalies() function only

uses the maximum value when multiple values are provided. Therefore,

setting level = c(90, 95, 99), for example, is equivalent

to setting level = c(99), which is the default value.

anomalies <- nixtla_client_detect_anomalies(df) # level=c(90,95,99)

#> Frequency chosen: h

head(anomalies) # only the 99% confidence level is used

#> unique_id ds y anomaly TimeGPT TimeGPT-lo-99

#> 1 BE 2016-10-27 00:00:00 52.58 FALSE 56.07206 -28.58840

#> 2 BE 2016-10-27 01:00:00 44.86 FALSE 52.41392 -32.24654

#> 3 BE 2016-10-27 02:00:00 42.31 FALSE 52.80694 -31.85352

#> 4 BE 2016-10-27 03:00:00 39.66 FALSE 52.58330 -32.07716

#> 5 BE 2016-10-27 04:00:00 38.98 FALSE 52.66963 -31.99083

#> 6 BE 2016-10-27 05:00:00 42.31 FALSE 54.10218 -30.55829

#> TimeGPT-hi-99

#> 1 140.7325

#> 2 137.0744

#> 3 137.4674

#> 4 137.2438

#> 5 137.3301

#> 6 138.76264. Plot prediction intervals

nixtlar includes a function to plot the historical data

and any output from nixtlar::nixtla_client_forecast,

nixtlar::nixtla_client_historic,

nixtlar::nixtla_client_detect_anomalies and

nixtlar::nixtla_client_cross_validation. If you have long

series, you can use max_insample_length to only plot the

last N historical values (the forecast will always be plotted in

full).

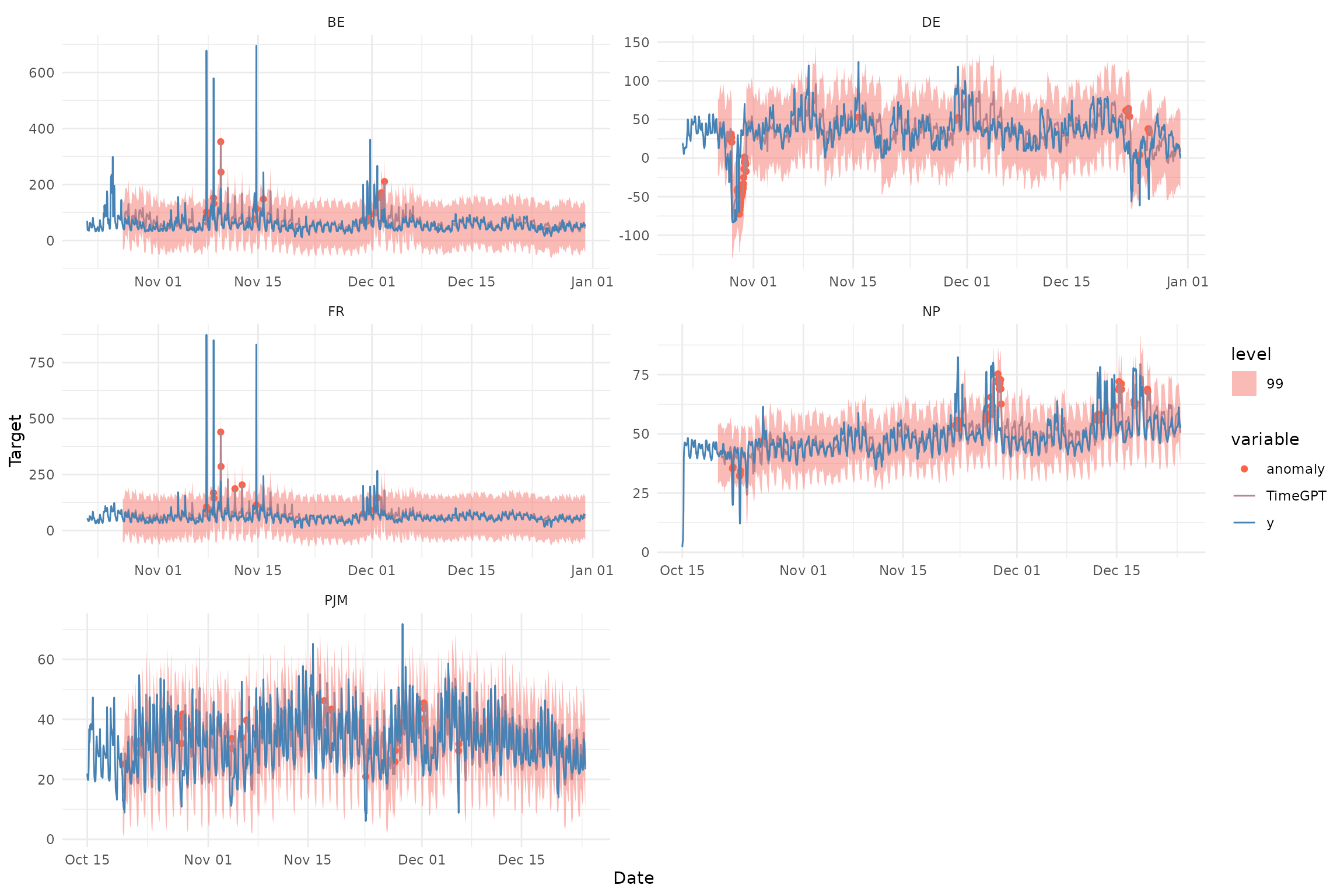

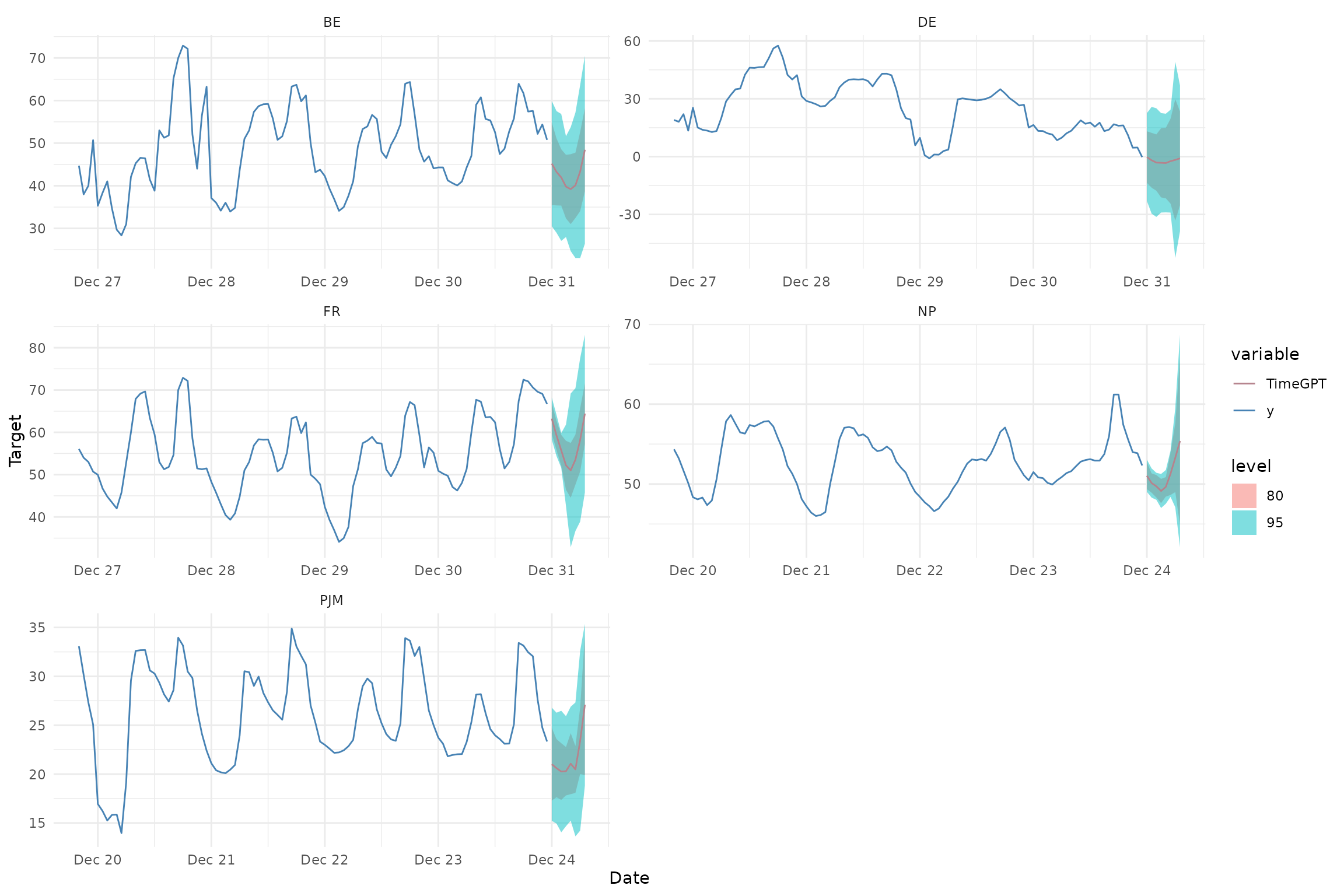

When available, nixtlar::nixtla_client_plot will

automatically plot the prediction intervals.

nixtla_client_plot(df, fcst, max_insample_length = 100)

nixtlar::nixtla_client_plot(df, anomalies, plot_anomalies = TRUE)